Germany is rapidly establishing itself as one of Europe’s leading AI hubs, powered by a fast-growing market, strong government investment, a thriving startup ecosystem, and massive infrastructure build-outs by global tech giants.

The country’s AI market is forecast at more than €9 billion in 2025 and is projected to grow to €37 billion by 2031, representing an annual growth rate of over 26%. With 935 AI startups, over €2 billion in venture funding deployed in 2025 alone, and a €5.5 billion High-Tech Agenda, Germany’s AI ambitions are backed by concrete capital and policy momentum.

Germany AI Industry Market Size and Growth Projections

Germany’s AI market is one of the fastest-growing in Europe, though estimates vary across research firms depending on scope and methodology.

| Source | 2024 Value | 2025 Value | Projected Value | CAGR |

| Fortune Business Insights | $10.04B | $12.18B | $54.71B (2032) | 23.9% |

| Grand View Research | — | $29.67B | $203.89B (2033) | 26.3% |

| GTAI / Statista | — | €9B+ | €37B (2031) | ~26% |

| Market Research Future | $5.85B | $7.63B | $110.03B (2035) | 30.5% |

The generative AI segment specifically is growing even faster. The German generative AI market generated revenue of $959.1 million in 2025 and is expected to reach $14.47 billion by 2033, reflecting a CAGR of 41.3%. This sub-sector is driven by enterprise adoption in natural language processing, computer vision, and predictive analytics.

Germany AI Startup Ecosystem

Startup Count and Growth

Germany’s AI startup landscape has expanded significantly. According to the appliedAI Institute for Europe’s 2025 Landscape report, there are now 935 AI startups in Germany — a 36% increase from 687 in 2024. This growth mirrors the previous year’s rate of 35%, signaling sustained momentum in the ecosystem. The survival rate of AI startups exceeds 90%, far higher than non-AI startups.

Funding Landscape

- Over the last decade, German AI startups received approximately €7.57 billion in total funding.

- In 2025 alone (through July), more than €2 billion was invested in German AI startups.

- 124 startups received funding exceeding €10 million — an increase of over 50% compared to 2024.

- Among startups with significant funding (>€1M), the average amount was €19.2 million and the median was €5.1 million.

- Newly founded AI startups (2023–2024) received approximately €260 million in cumulative funding, nearly triple the €93 million for the 2022–2023 cohort.

AI was the top industry by number of deals in Germany in 2025, with 30 deals and $544.64 million raised.

Geographic Distribution

Berlin and Munich dominate, together accounting for nearly 50% of all AI startups.

| City/Region | Number of AI Startups | Share |

| Berlin | 283 | 30.3% |

| Bavaria (Munich + suburbs) | ~236 | 25.2% |

| Baden-Württemberg | — | 11.7% |

| North Rhine-Westphalia | — | 9.8% |

| Hamburg | 71 | 7.6% |

| Hesse | — | 6.0% |

Six federal states account for over 90% of all German AI startups. Berlin and Munich also rank among the world’s top 11 VC destinations for agentic AI, occupying third and eleventh spots respectively.

Generative AI Startups

Every third German AI startup (316 out of 935) is now active in the field of generative AI — a growth rate of approximately 130% compared to the previous year. This signals a rapid shift from niche technology to a core driver of innovation.

Germany AI Government Policy and Investment

National AI Strategy

Germany adopted its National AI Strategy in November 2018 and initially committed €3 billion for AI R&D through 2025. This was later increased to €5 billion through the economic stimulus package. The strategy focuses on making Germany a leading AI research center, deploying AI responsibly, and integrating AI into society in ethical and legal terms.

High-Tech Agenda 2025

The federal government’s High-Tech Agenda 2025 identifies AI as one of six key technologies and sets the ambitious goal of generating 10% of domestic economic output from AI-based activities by 2030.

A €5.5 billion policy initiative supports next-generation intelligence models, increased computing capacity, and data infrastructure with a focus on industrial applications. Flagship knowledge transfer projects for key industries — automotive, chemicals, biotechnology, cleantech, medicine, and agrifood — will launch from 2026 onward.

Digital Ministry (BMDS)

Germany’s new coalition government created the Federal Ministry for Digital and Government Modernization (BMDS) to centralize AI strategy, open data, and infrastructure initiatives. The government has pledged to spend at least 3.5% of GDP annually over five years on critical technologies, including AI, quantum computing, and robotics.

Modernization Agenda

Chancellor Friedrich Merz’s cabinet approved a modernization agenda that integrates AI into government and public services — including export regulation platforms, visa processing, and court operations.

Enterprise AI Adoption in Germany

AI adoption among German companies is accelerating but remains uneven across company sizes.

- By June 2025, 40.9% of German companies were using AI, according to a business survey.

- A separate IW survey of 1,038 companies found 37% currently use AI, with large companies (66%) far ahead of small companies (36%).

- More than 70% of businesses in Germany are planning to invest in AI in 2025 for data analytics, process automation, and new product development.

- Over half of firms surveyed use generative AI or expect to use it by end of year, up from 26% in 2024.

- GenAI-related spending is expected to rise from 0.3% of aggregate sales in 2024 to 0.5% in 2025 and 0.8% in 2026.

Mittelstand Challenge

Germany’s small and medium-sized enterprises (Mittelstand) are falling behind. These firms allocated only 0.35% of revenues to AI in 2025, down from 0.41% in 2024 — approximately 30% below the overall market average of 0.5%. Geopolitical uncertainty, cost optimization pressures, and early AI investments not yielding expected efficiency gains have contributed to this decline. Bureaucratic obstacles and data protection concerns further hinder mid-sized firm adoption.

Job Impact Expectations

More than a quarter of German companies (27.1%) expect AI to lead to job cuts within the next five years, while only 5.2% anticipate additional jobs and two-thirds expect no change.

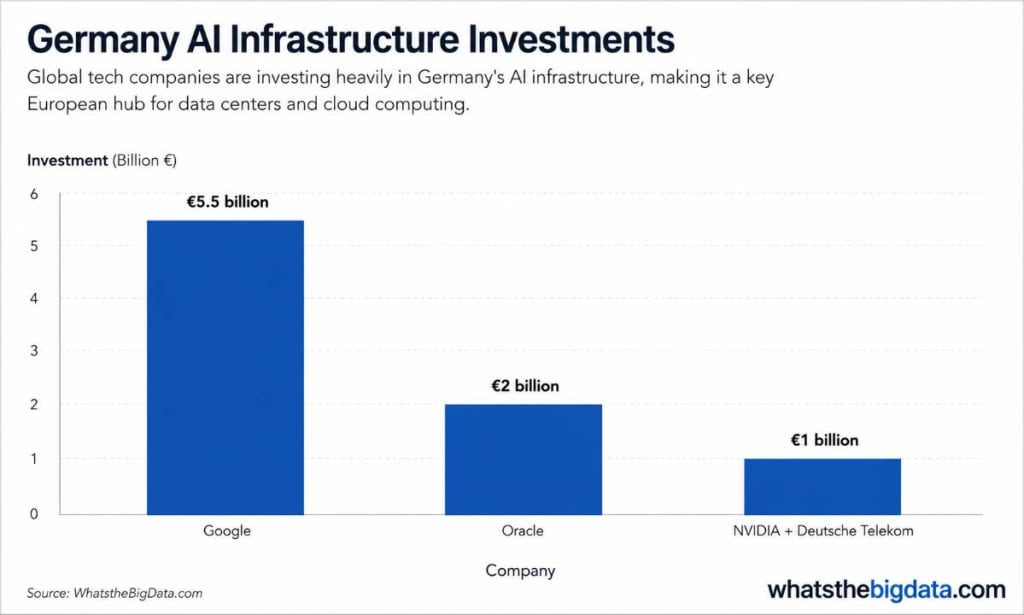

Germany AI Infrastructure Investments

Global tech companies are investing heavily in Germany’s AI infrastructure, making it a key European hub for data centers and cloud computing.

| Company | Investment | Timeframe | Details |

| €5.5 billion | 2026–2029 | New data center in Dietzenbach; expanded offices in Berlin, Frankfurt, Munich | |

| NVIDIA + Deutsche Telekom | €1 billion | Operational Q1 2026 | One of Europe’s largest AI data centers |

| Oracle | $2 billion | 5 years | AI and cloud infrastructure expansion, Frankfurt Cloud Region |

The AI data center market in Germany was valued at $1.78 billion in 2025 and is projected to reach $10.44 billion by 2031, posting a 34.28% CAGR driven by GPU deployments and sovereign-cloud mandates. Two AI factories are currently active in Germany: HammerHAI in Stuttgart and JUPITER AI Factory (JAIF) in Jülich — the fastest supercomputer in Europe and the first exascale computer.

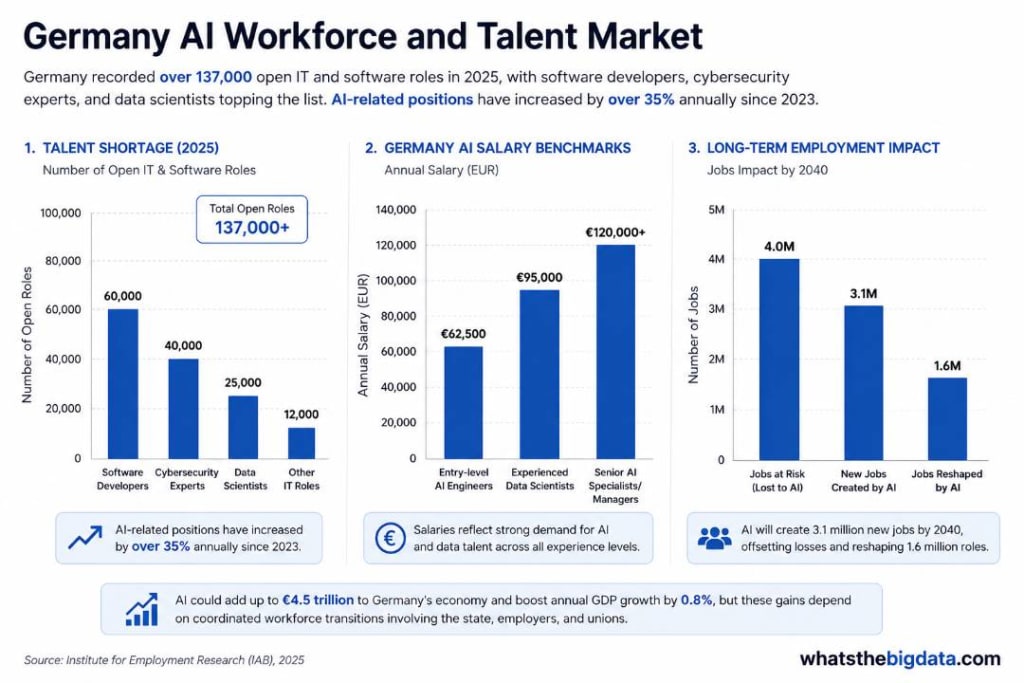

Germany AI Workforce and Talent Market

Talent Shortage

Germany recorded over 137,000 open IT and software roles in 2025, with software developers, cybersecurity experts, and data scientists topping the list. AI-related positions have increased by over 35% annually since 2023.

Germany AI Salary Benchmarks

| Level | Annual Salary (EUR) |

| Entry-level AI Engineers | €55,000–€70,000 |

| Experienced Data Scientists | €80,000–€110,000 |

| Senior AI Specialists/Managers | €120,000+ |

Long-Term Employment Impact

The Institute for Employment Research (IAB) projects that Germany will lose 4 million jobs to AI by 2040 while creating 3.1 million new ones, resulting in a net gap of approximately 900,000 positions. An additional 1.6 million jobs will be significantly reshaped.

AI could add up to €4.5 trillion to Germany’s economy and boost annual GDP growth by 0.8%, but these gains depend on coordinated workforce transitions involving the state, employers, and unions.

Germany AI Research and Academic Ecosystem

Germany boasts a world-class AI research infrastructure. The country is home to Cyber Valley, Europe’s largest consortium for research and innovation in machine learning.

Top AI Universities

- Technical University of Munich (TUM)

- RWTH Aachen University

- Karlsruhe Institute of Technology (KIT)

- University of Freiburg

- University of Munich (LMU)

- Heidelberg University

- Darmstadt University of Technology

- Technical University of Berlin

- University of Stuttgart

- University of Hamburg

Key Research Institutions

- German Research Center for Artificial Intelligence (DFKI) — one of the world’s largest AI research institutes.

- Fraunhofer Institutes — applied AI research across manufacturing, healthcare, and logistics.

- National AI Competence Centers — federally funded centers for strengthening AI research excellence, with doubled funding through 2022.

- JUPITER AI Factory in Jülich — Europe’s fastest supercomputer and first exascale computing system.

Key Industry Sectors for AI

AI is being deployed as a cross-sectional technology across Germany’s economy, with concentration in several key verticals.

| Sector | Role in AI Market | Notable Applications |

| BFSI (Banking, Financial Services, Insurance) | Largest market share | Fraud detection, risk assessment, automated consulting |

| Healthcare | Fastest-growing CAGR | Diagnostics, personalized medicine, drug discovery |

| Manufacturing | Core to Industry 4.0 | Predictive maintenance, quality control, process automation |

| Automotive | Major investment area | Autonomous driving, driver-assistance systems, smart manufacturing |

| Cross-Industry Applications | Most startups (158) | Enterprise tools, data analytics, customer service |

Among AI startups specifically, cross-industry solutions lead (158 startups), followed by healthcare (110), manufacturing (88), and transportation/mobility (51).

Challenges and Risks

Despite strong momentum, several challenges persist in Germany’s AI trajectory:

- Mittelstand gap: SMEs are cutting AI spending while larger firms accelerate, creating a growing digital divide.

- Talent shortage: Over 137,000 unfilled IT positions reflect a structural skills gap that limits AI deployment.

- Regulatory concerns: While 73% of companies believe clear AI regulations can offer a competitive advantage, uncertainty around the EU AI Act and data protection rules continues to slow adoption in some sectors.

- Scaling difficulty: Many AI startups struggle to secure late-stage funding, and limited access to international markets hinders the transition from small ventures to globally competitive tech players.

- Energy infrastructure: The AI data center boom is pushing the power grid to its limits, creating tension with Germany’s climate goals.

- Superficial adoption: Most companies predominantly use free AI tools rather than purchasing or developing proprietary solutions, indicating that overall AI adoption is still relatively shallow.